Market Outlook & Buying Strategy

Executive Summary

Global freight indices weakened modestly this past week, while Chinese factory pricing for newbuild containers remained stable despite elevated inventories and subdued order volumes. This divergence creates a tactical buying window—particularly on the U.S. West Coast, where market pricing remains competitive and supply is balanced. Inland pricing premiums continue to be driven by repositioning costs rather than structural scarcity.

Recommendation

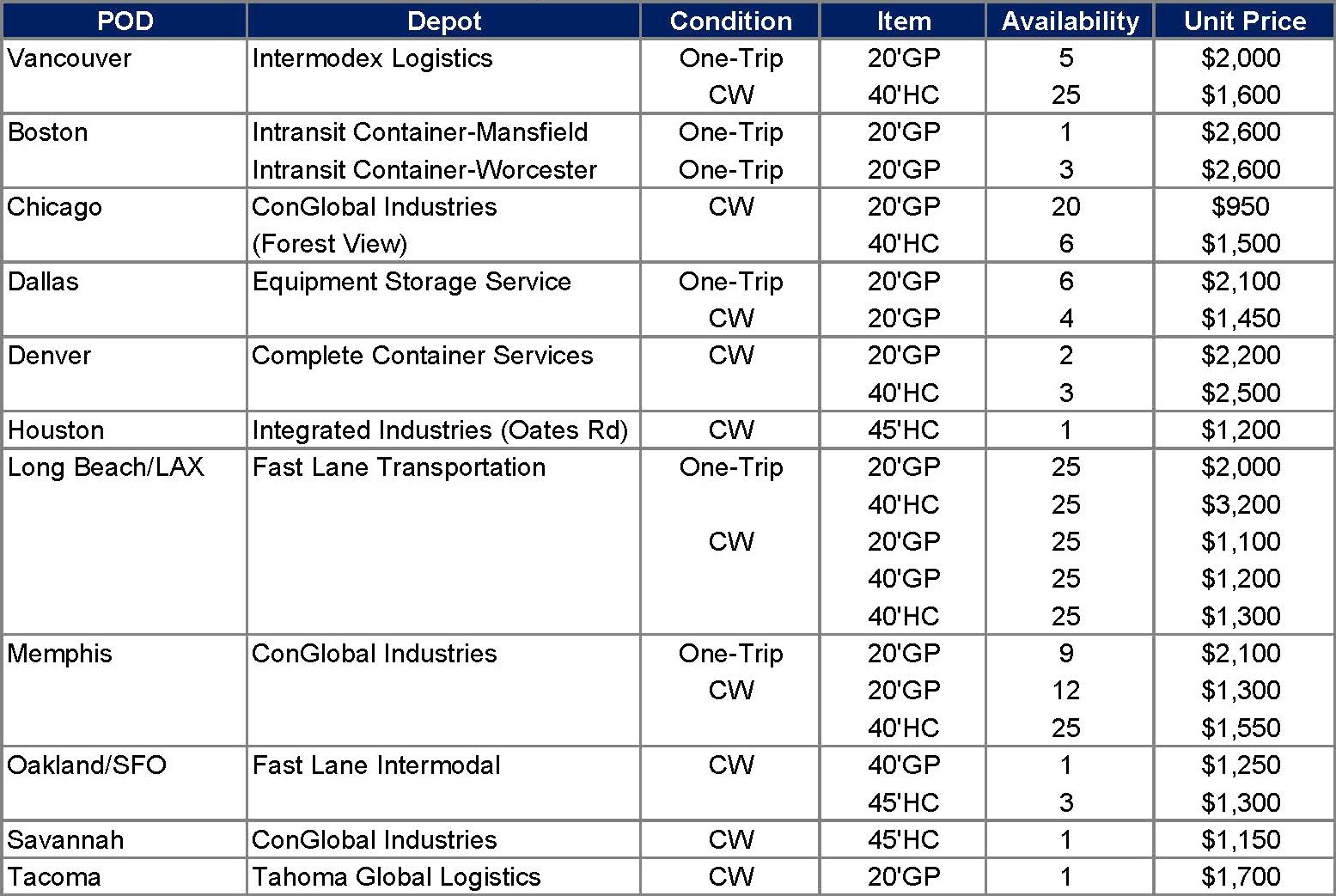

We recommend immediate procurement of 40HC CW units across West Coast depots, where pricing remains below effective replacement cost after handling and inland transport are included. Selective acquisition of one-trip 20GP units in the same region is also encouraged due to favorable availability and cost efficiency.

High-priced inland markets should be approached selectively, with bulk procurement deferred in favor of repositioning from coastal inventories when economically justified.

Market Summary

Global Freight and Macro Indicators

Table 1. Key Freight Benchmarks – Latest Readings

| Index | Latest Level | W/W Change | Comment |

|---|---|---|---|

| Drewry WCI (US$/40ft) | 1,806 | -2% | Softness across Transpacific and Asia–Europe |

| FBX Global Index | 1,799.75 | Slightly lower | Stabilizing but subdued rate environment |

| SCFI Composite | 1,393.56 | -3.98% | Third consecutive weekly decline |

Macro Context

United States: PMI results diverged, with S&P Global at 51.9

(expansion) and ISM at 48.2 (contraction).

Eurozone: Manufacturing slipped to 49.6, reflecting continued

inventory reduction and weaker factory activity.

China: Private-sector PMI fell to 49.9.

China Factory Conditions

- 2026 output forecast: 2.0–2.5M TEU.

- Factory inventories: 1.68M TEU.

- One of the biggest steamship lines placed an order near 100,000 TEU, while most remaining orders fall in the 1,000–3,000 TEU range.

- Factory offers for 40HC one-trip: USD 1,490–1,550/TEU.

- Steel mill guidance points to upward input cost pressure into December.

Analytical Insights

Soft Freight vs. Sticky Factory Prices

- Large anchor orders by major carriers

- Rising material and production costs

- Selective discounting rather than broad cuts

Regional Demand Divergence

Inland markets continue to command premiums due to repositioning costs. Coastal depots offer the best blend of price, availability, and flexibility.

China Inventory Overhang

High inventories and sub-50 PMI readings suggest controlled production and selective discounting. This supports early procurement planning for Q1–Q2.

Outlook & Recommendation

4–6 Week Market Outlook

Freight rates expected to remain range-bound into mid-December, with slight firming possible before Lunar New Year shipments begin accelerating.

Final Recommendation

Muwon USA should secure West Coast 40HC CW and one-trip 20GP inventory now, while delaying bulk inland purchases in favor of repositioning from coastal supply.